What are Mutual Funds? Basic terms associated with MFs

Types of Mutual Funds

Where and how to invest?

Deciding a fund for yourself

Taxation and good strategies

What are Mutual Funds

A mutual fund is a company that pools money from many investors and invests the money in securities such as stocks, bonds, and short-term debt. The combined holdings of the mutual fund are known as its portfolio. Investors buy shares in mutual funds. Each share represents an investor’s part ownership in the fund and the income it generates

https://www.paytmmoney.com

Why should you buy a MF?

Professional management

Diversification: The AMC investing in money markets, debts, bonds, even NASDAQ on your behalf

Affordability: With a small fee you can continue with your day job

Liquidity: Most funds charge no exit fee if you exit after 7 days. Taxes are also low compared to FDs if MFs are held for longer periods

Segregation: You can invest according to your future objectives

And also to avoid this.

Common terms associated with MFs

NAV (Net Asset Value): Put simply, this is the price at which you can buy a unit of mutual fund at. Specifically, it is the per unit value of net assets (value of their holdings, cash and cash equivalents, among others) and liabilities (short-term payments, expenses, etc)

AMC: A company that pools money from investors. The pooled money is then invested in different in different schemes that they provide. IDBI, Axis, Nippon, Aditya Birla Sunlife, ICICI Prudential are some of the examples

Expense ratio: (Total costs involved in running a fund/Total assets of that fund). These are directly deducted from daily NAVs and don’t reflect as a specific charge to investors

if you invested $10,000 in a fund with a 10% annual return, and annual operating expenses of 1.5%, after 20 years you would have roughly $49,725. If you invested in a fund with the same performance and expenses of 0.5%, after 20 years you would end up with $60,858

Exit load: This is a penalty that an AMC might charge when an investor decides to prematurely exit from its fund. For example, a fund with 1% exit load for withdrawals before a year would charge 1% of your NAV (NAV at time of withdrawal) if you redeem your investments after 6, 7 or 8 months

Ways to invest

Regular: You invest in mutual funds via your broker. The broker directly deal with investments and you pay a small amount to her/him to manage your portfolio

Direct: You pay the money directly to the AMCs or via a low to no cost agency like Coin by Zerodha, PayTM money or ET money. These plans have lower expense ratios when compared to regular plans as there are no distribution costs

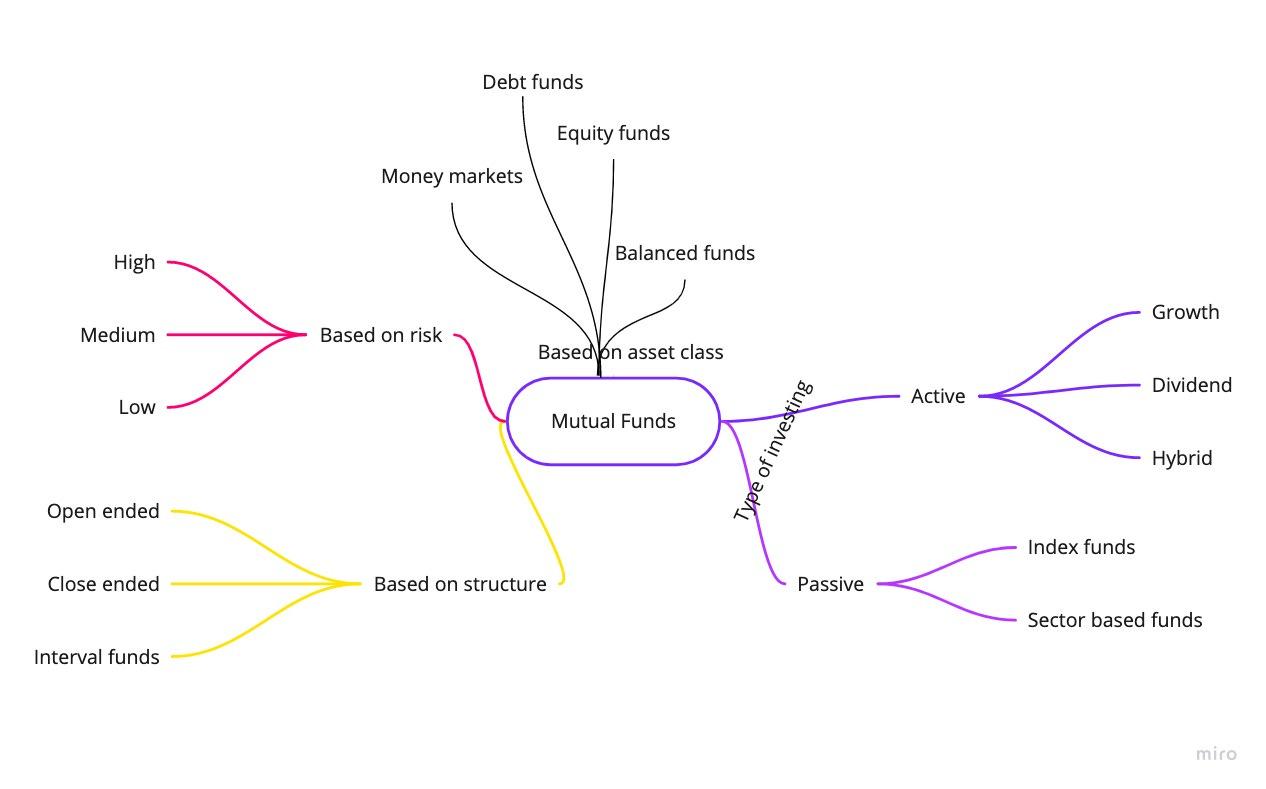

Active: The fund manager takes a hands-on approach, does research and take full advantage of market fluctuations in a bid to beat the market. ER is higher in these cases

Passive: In this the fund mirrors an index or sector and the returns are near to the returns that are offered by indices or sectors

Types of Mutual Funds

https://www.whatgaurav.com/

Basics

Equity based funds: Funds that invest more than 65% of their money in equity. All other funds are classified as non equity based funds in India

The core of finance is “High risks, high returns” and “Long term beats short term deviations and to a certain extent tail risks”

Growth funds are preferred for wealth creation, dividend funds for regular income and liquid funds for parking your money temporarily (30 - 60 days)

SIPs are systematic investment plans that allow you to deposit a certain amount on regular intervals. Lumpsum is when you make a one-time investment

Based on structure

Open ended funds: These are the funds in which investments and redemptions can be made throughout the year. These are ideal for those who want liquidity with no restrictions on maturity periods

Close ended funds: CEs can only be purchased via NFO (new fund offering). They can be bought or sold only for a few days after the launch. Post this they are traded in secondary market and are bought and sold like stocks. The mandate for these funds end after their maturity period

Interval funds: These funds can be bought or sold on specific dates only - like bid on 5th of every month and redemption only on 25th. These might be listed on bourses

Based on asset class

Equity funds: These funds have a mandate to invest in securities listed in the market. These are high risk, high return funds

Large cap: These funds choose stocks which are relatively stable. These are safest option amongst equity funds

Mid cap/ small cap: Investments basis the range of market capitalisation that a company falls in. Small cap funds are amongst the riskiest in the market

Multi cap: These funds have a mandate to invest in any and all the companies they deem suitable given the portfolio fulfils investors objective

Debt funds: These invest in, as the name suggests, debt - company debentures, government bonds and other fixed income instruments

Liquid funds: These funds invest in commercial papers, government bills, essentially all g-secs and instruments that have a maturity date of less than 91 days. These are not wealth-generating funds but can be considered for parking your money on short term basis. These can be redeemed even within a day and are typically better than FDs

Ultra short term/ other funds: These funds invest in corporate bonds or other similar debt instruments basis their maturity periods and inherent risks

Balance or hybrid funds: These funds invest in a mix of asset classes to balance out risk and reward. A fund might have say 60 - 80% in equities and 20 - 40% in debt (e.g., Franklin India Balanced Fund)

Solution based funds

Growth funds: These funds have an objective of capital appreciation. They typically invest all the dividends in the fund back and provide a better NAV. These are riskier options but recommended if you are starting out early

Income funds: These funds provide you regular incomes either via dividends or interests they earn on debt instruments. Good if you need additional money apart from my monthly earnings

ELSS: These funds have a lock-in period of 3 years with investments in equities. You cannot redeem investments in ELSS before the lock-in period. Investments upto ₹1.5 lakhs are eligible for tax benefits under 80C of the Income Tax Act

Others: pension funds, capital protection funds, fixed maturity funds

Specialty funds

Sector Funds: These are funds that invest in a particular sector of the market e.g. Infrastructure funds invest only in those instruments or companies that relate to the infrastructure sector. Returns are tied to the performance of the chosen sector. The risk involved in these schemes depends on the nature of the sector

Index Funds: These are funds that invest in instruments that represent a particular index on an exchange so as to mirror the movement and returns of the index e.g. buying shares representative of the BSE Sensex

Fund of funds: These are funds that invest in other mutual funds and returns depend on the performance of the target fund. These funds can also be referred to as multi manager funds. These investments can be considered relatively safe because the funds that investors invest in actually hold other funds under them thereby adjusting for risk from any one fund

Where and How to Invest

(Below are my personal preferences only)

Always invest in direct plans. Expense ratios suck a lot of money from you in long term. Investment can be made via RTGS/NEFT/UPI directly by going to an AMC’s website

*Demo in class*

For better management, apps like PayTm Money, Coin by Zerodha, Groww, ET money provide low to NIL cost investing options. But if they don’t charge you anything, how do they earn money?

*Demo in class*

Now How?

KY: Know yourself. First ask two basic questions.

What’s your horizon? Do you want this money in next 2 years, next 10 years or you really don’t care? Also, is this for your marriage, you child’s education or a trip you are planning?

What’s your risk appetite? Does it give you the heebie jeebies when the market corrects (goes down) or flinch and take the investments out or you stayed calm even during COVID when the market threw tantrums

Analysis

Below metrics can be looked into -

Performance against NIFTY/ SENSEX or any relevant benchmark

Performance against category

The 3x3 matrix to validate if the fund meets your objective

Consistency and size of the AUM

Asset allocation and your trust in the companies in the portfolio

Expense ratio and exit load if you have a short-term horizon

STCG: Short term capital gains for investments withdrawn before 1 year for equity based funds and before 3 years for other funds. Always applied on SIP or lumpsum on FIFO basis (investments made first are withdrawn first)

LTCG: Long term capital gains are when investments are kept for more than a year for equity based funds and for more than 3 years for other funds. Taxes are again always applied on FIFO basis

Indexation: This provides the benefits of inflation on taxes. The inflation growth between bid and redemption is deduction from the tax rate for non equity based funds in case of long term gains

*Grandfathering cause applies in case you had investments before 31st January 2018. We will not study that in depth for the benefit of class. However, you can refer the same with some pretty neat examples here.*

Strategies

These are pretty much the basics, but are nevertheless important for investing of any kind. Follow below

KYY: Know your risk appetite and time horizon for investment

Never keep all your eggs in one basket. Diversify

If possible, stay long term. On an average only 1% of day traders can beat returns from a low cost ETF

Don’t go for an overlapping portfolio. If you have SENSEX 50 SBI Index fund in your portfolio, then it doesn’t make sense to go for a similar index fund with ICICI. Why take that risk?

If you are young, go for growth options and look for wealth generating schemes