Real-Time Payments

A primer on the workings of the most revolutionary payment system out there.

Real-Time/ Instant/ Faster Payments in its most stripped-off definition is the transfer of funds (money) from A to B instantaneously. A and B can be a person or a business.

RTPs are you scanning a QR code to pay for that orange you bought at the grocery store or the funds that you sent to your friend for that lunch money (s)he loaned you. Essentially, any financial transfer that happens within seconds.

That’s it. I’ll go on a limb and assume that you know the ‘What’ of RTPs. So, in this piece, we are going to double click on how real-time payments happen, the intermediaries that make it happen, and why they are so happening!

To make this piece as comprehensive as possible, I will take the example of you buying the most orange orange on Amazon, paid for via UPI (Unified Payments Interface: RTP payment form in India).

But before we start, let me introduce you to the main characters in the RTP flow.

Virtual Payment Address (VPA/ also called UPI ID with love) is a unique identifier of your bank account. Your name, bank account number, bank branch, and other details are encrypted to a VPA. A UPI transfer can be done only with a VPA. Examples can be myorange@citibank or needmymoneyback@upi

You: The one who fell in love with them oranges

Merchant: Seller - Amazon in our example

Acquiring bank: Merchant’s bank. Also called as sponsor/ payee/ beneficiary bank

Issuing bank: Your bank. Also known as destination/ remitter/ payer bank

Network Operator: The entity responsible for facilitating payments. Every transaction passes via this nodal authority. They act as intermediaries and facilitate the authorisation, clearing, and settlement of transactions Examples: NPCI, RBI, Fed. In case of credit/ debit card transactions, this role is assumed by entities such as Visa, Mastercard, Discover and the like

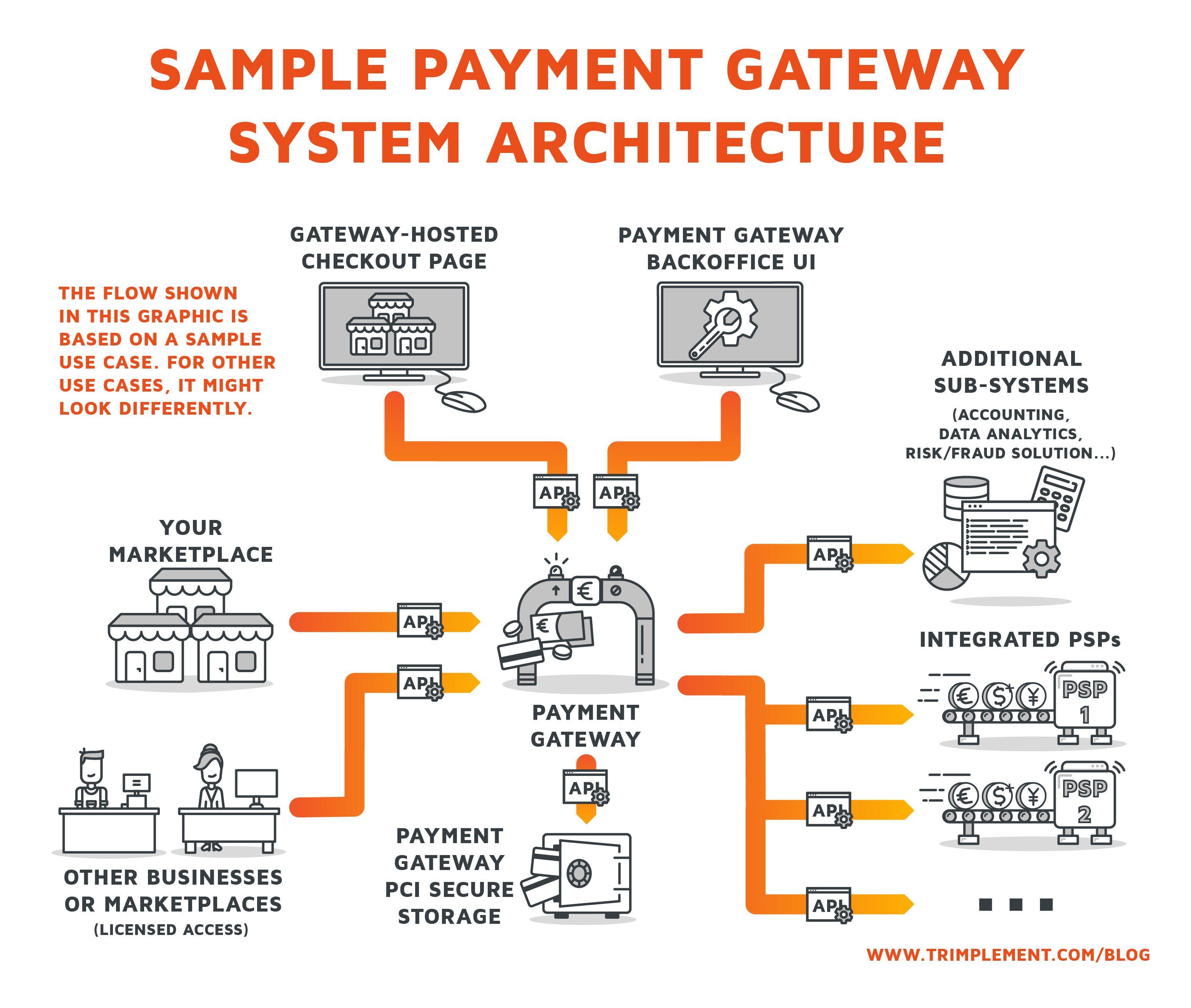

Payment Gateway: The entity responsible for providing the required tech infrastructure for various types of payments. A PG also tokenizes/ encrypts payments details, does fraud checks, among other things. Amazon can either be a PG (Amazon Pay) or use services of other PGs (Stripe, Instamojo, CCAvenue, Braintree). In our example, PG would be Razorpay

Payment Aggregator: A PA allows merchants to accept payments from customers by integrating with their websites or Apps and then settle that to the merchants as per agreed-upon timelines. In short, it provides a sub-merchant account. Banks used to dominate the PA market before but most tech players have made inroads now. Examples: Cashfree, Paypal, Amazon Pay

Payment Service Providers or Third-Party Application Providers (PSPs/ TPAPs): A PSP is responsible for maintaining customer details, transaction logs, and for issuing, maintaining, and resolving VPAs. These are players like Google Pay, Apple Pay, PhonePe, PayTm who have an application layer (UI) for client interactions and a backend to manage the above mentioned activities. The backend layer is also known as a PSP backend

Only banks and approved technology partners can act as PSP backends and can interact with the operator. Having a standalone PSP backend or frontend makes no business sense and hence most PSPs act as one single unified entity with banks backing them up. PSPs such as PhonePe, BHIM, Gpay provide both frontend and backend facilities

Note: You’d hear names like Razorpay, Stripe, Paypal, Adyen, PayTm also being referred to as PSPs. This is because PSP is a generalized name used for PGs + PAs (entities providing payment services). Gpay, PhonePe are UPI PSPs which for all intents and purposes can work with, say, Stripe to provide a rich UX to customers.

The Flow

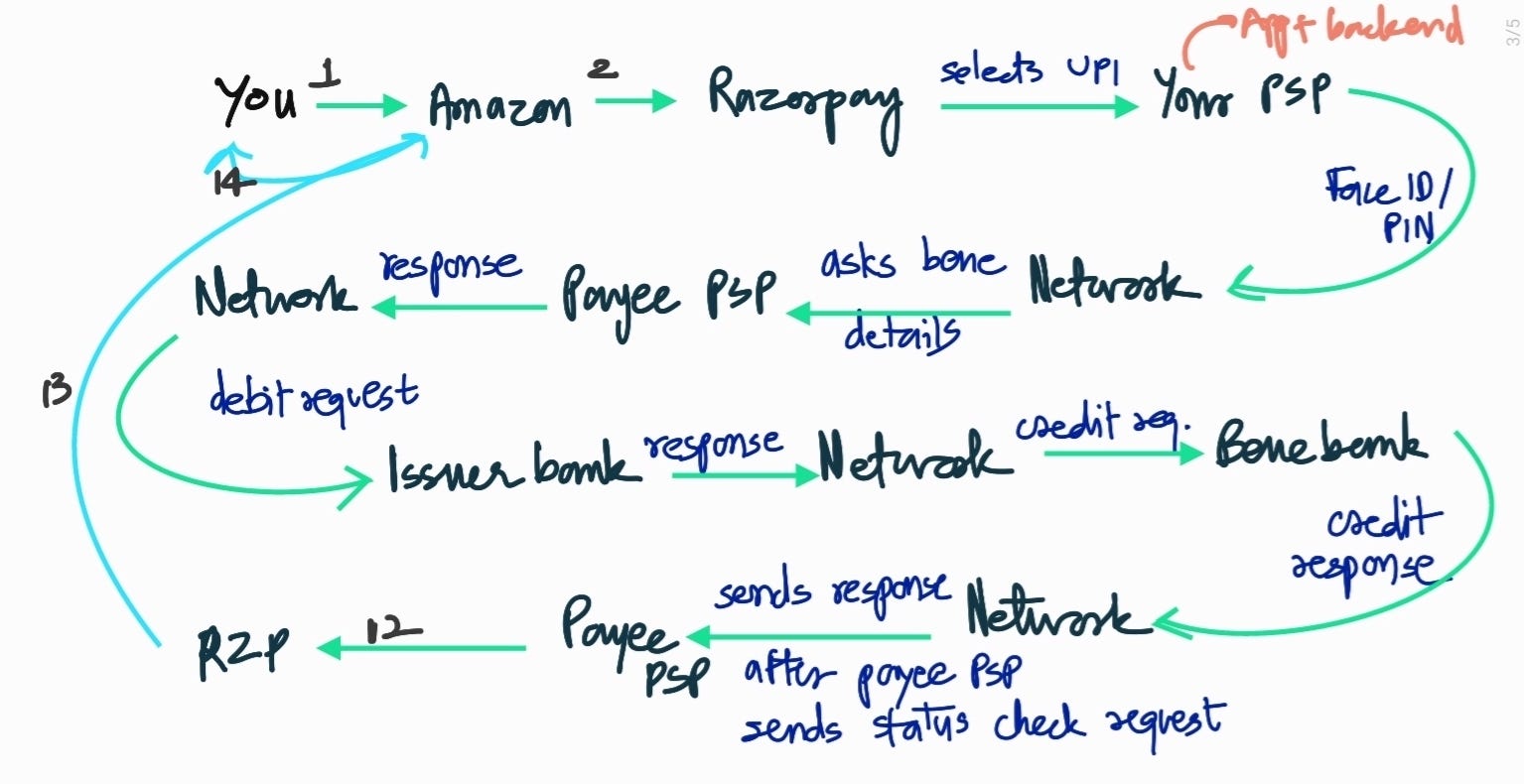

You go to the seller app, select orange, go to the checkout page and opt for ‘place order and pay’

The merchant website redirects you to a PG (Imagine Razorpay here) with multiple options to pay: cards, net banking, wallets, RTP/ UPI (Imagine BHIM, PhonePe, Google Pay). You opt for Gpay. You can access UPI payment modes by either providing your mobile number or VPA

The PG forwards the request to your PSP (Gpay here). Gpay then authenticates your details. As per RBI guidelines in India, TPAPs have to follow a two-factor authentication (2 FA). The first factor can be decided by the provider (imagine FaceID/ PIN/ Biometrics to login to the App), but the second factor is defined by the nodal authority (UPI PIN/ MPIN)

The PSP backend of Gpay forwards the verified request to the network operator

The network operator then sends the payment request to the payee PSP for resolution of beneficiary VPA/ address

Upon resolution of bene address by the Payee PSP, the operator sends the debit request to the issuing bank

The issuing bank sends the success/ failure response of the debit request to the operator. Considering how much you love oranges, we shall assume that the payment is a success

The operator accepts the success response and furthers a credit request to the beneficiary bank

The bene bank sends a successful credit message to the network. The Payee PSP sends a status check request to the network, which gets responded with a success in our case

The payee PSP forwards the success message to the payment gateway. The PG sends that to the Merchant

The merchant shows a Hurray message to you and asks you to wait for them Oranges

Scratching the Surface

Now, I just named the whole process ‘The Flow’, but the overall transaction cycle doesn’t end here. The flow described above is just the authorization cycle. This means that the merchant’s and your bank only got a confirmation of the transaction and the actual money never got transferred between banks. The banks credited the money to you from their accounts with a trust that they will get the consolidated funds from the operator later on.

Confused? Let me explain. In 2021, we had an average of 120 UPI transactions every second. Now transferring money at such a frequency is a massive challenge (compare this against 1 bitcoin transaction taking approximately 60 minutes to get completed). But confirmations can flow smoothly (take your text messages on WhatsApp). Hence, the actual USP of UPI is in the mechanism wherein it allows payers and payees to act on messages and transfers actual funds (by netting the debit and credit positions of the banks) at predefined cycles later on.

The process of clearing (computing which bank owes how much and the net amount) happens in real-time. You can imagine this as passing debit and credit entries against banks in a ledger after every transaction. At the time of settlement, the operator forwards the file with net positions against the banks to the financial institutions. Banks then settle the funds amongst themselves. For UPI in India, the actual settlement happens only 8 times in a day.

In case you are wondering about what happens when a bank defaults and says, ‘though you have got your oranges but I ain’t paying for it later!’, then fret not. The operator usually has a settlement guarantee fund to honor the commitments of other banks. But this thread is not about SGFs and settlement risks, so let’s stop here.

Modalities for Further Reading

I understand that there was a lot of unpack, but in case you were observant enough, you’d have questions such as:

When do these payments time-out? 90s, 120s?

How request and response messages are sent, at what frequency, and for how long?

Does the VPA act as my public key for RTP transfers?

Which payment mode is used for gross settlement of funds?

What is a settlement guarantee fund? What other risks do RTPs pose?

Also, what happens when the communication link (REST APIs in XML) breaks between the operator, PSPs, PGs, and banks?

Does a payment aggregator use escrow account to settle payments to merchants?

What are the charges involved? Do interchange, switching, PSP Fees/ MDR apply to?

How does QRs and POS machines fit into the RTP ecosystem?

And though these problems are super exciting and have quite innovative solutions; for now, they fall outside the scope of this thread. But if you are curious enough, drop me a line!

Links for Further Reading

https://www2.deloitte.com/content/dam/Deloitte/us/Documents/strategy/us-cons-real-time-payments.pdf

https://www.forbes.com/sites/boblegters/2022/02/10/why-all-the-fuss-about-real-time-payments/?sh=355e39bb3d4c

https://en.wikipedia.org/wiki/List_of_online_payment_service_providers

Popular PGs

caption... Sample PG System Architecture

https://razorpay.com/blog/what-is-upi-and-how-it-works/

Real time cross border payments